TLDR;

This video provides a four-step guide to help viewers decide whether to rent or buy a house, challenging common myths and focusing on financial analysis. It emphasises the importance of mindset, understanding housing myths, running the numbers with tools like the NYT calculator, and assessing personal financial readiness.

- Renting can be a financially sound decision.

- Many common beliefs about home ownership are myths.

- Running the numbers is crucial before deciding to buy.

- Financial readiness is key to a sound home-buying decision.

Step 1: Change Your Mindset Around Renting [0:42]

The first step involves accepting that renting can be a financially sensible option. Many people are conditioned to believe that renting is a waste of money, but this isn't always the case. Using the example of a condo in Palo Alto, California, which sold for $2.15 million in 2018, the video illustrates that renting the same unit for $5,400 a month is significantly cheaper than the estimated $13,106 monthly cost of owning it, even before considering additional "phantom costs" like maintenance and closing costs.

Step 2: Understand the Myths Around Housing [3:05]

This section addresses and debunks three common myths about housing. The first myth is that renting means you're just paying your landlord's mortgage. The video argues that landlords charge what the market will bear, not simply adding a profit margin to their costs. The second myth is that renting is throwing money away. The video counters this by stating that rent pays for value, such as a roof over your head and maintenance services, similar to paying for a meal at a restaurant. The third myth is that buying a house builds equity. The video explains that building equity takes a long time, and a significant portion of early mortgage payments goes towards interest rather than principal.

Step 3: Run the Numbers for Renting Versus Buying [9:22]

Before buying a house, it's essential to run the numbers and not rely solely on a broker's advice. The video highlights that many people underestimate the total cost of ownership (TCO), which includes closing costs, maintenance, opportunity cost, transaction costs, and renovations. Using the New York Times rent versus buy calculator, the video demonstrates that, for the Palo Alto property, renting saves over $800,000 over eight years when factoring in maintenance. Additionally, investing the down payment instead of using it for a house purchase could result in saving $1.1 million over eight years.

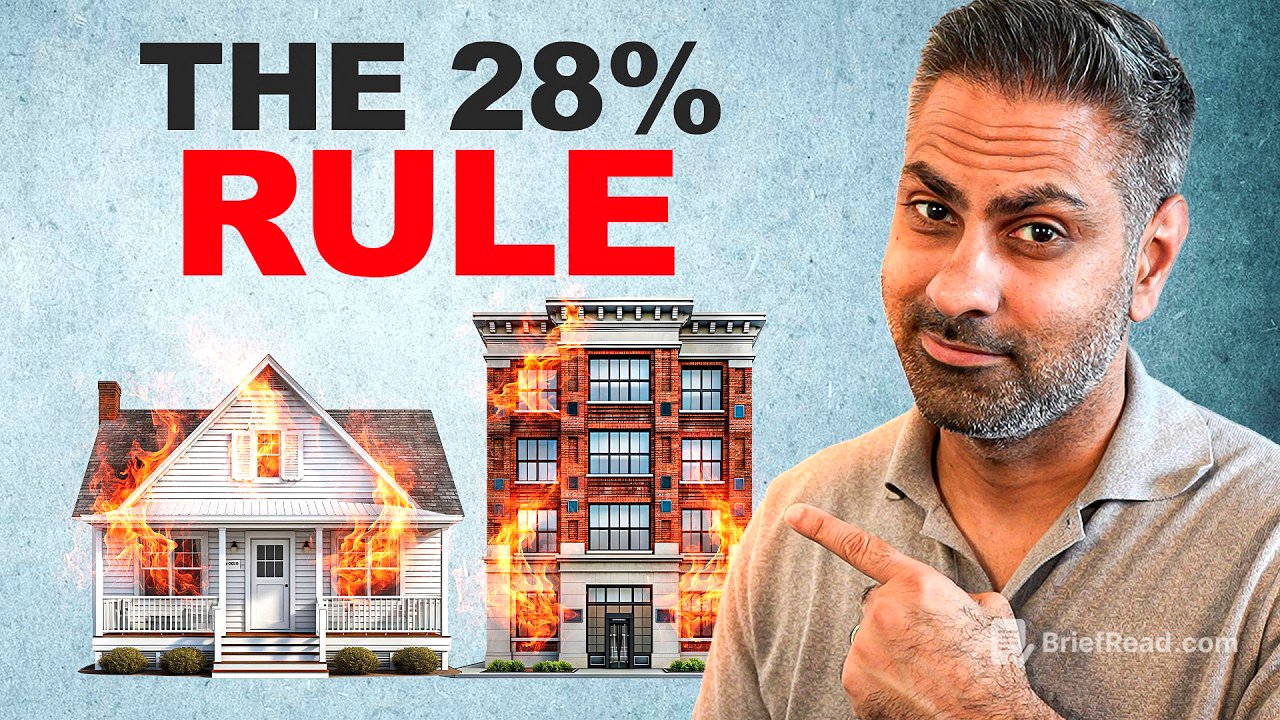

Step 4: Figure Out If You Are Ready to Buy [16:54]

This final step focuses on assessing personal financial readiness. The video introduces the 28/36 rule, which states that total housing costs should be less than 28% of gross monthly income, and total household debt should not exceed 36% of gross monthly income. It also emphasises the importance of saving a 20% down payment, not just for avoiding PMI (Private Mortgage Insurance), but for building a saving habit crucial for handling unexpected housing expenses. The video suggests that if you can't save 5-10% of your take-home pay and invest 10%, you're spending too much.