TLDR;

This video provides a three-step guide to setting up a family trust to protect and pass wealth through generations. It emphasizes the importance of fortifying the family by establishing an irrevocable trust, selecting trustworthy co-trustees and successor trustees, and funding the trust with tangible and digital assets, including life insurance. The guide also highlights the significance of financial literacy, legacy conversations, and structuring the trust to finance the future by building a strong financial statement and leveraging it for financial opportunities.

- Fortifying your family with an irrevocable trust and carefully chosen trustees.

- Funding the trust with tangible and digital assets, including life insurance.

- Structuring the trust to finance the future and build a strong financial statement.

Intro [0:00]

The speaker introduces the topic of setting up a family trust to ensure wealth lasts beyond multiple generations. He stresses the importance of structure and provides a three-step approach to establishing a family trust, emphasizing the need to protect the family and their assets.

Step 1: Fortifying Your Family [0:29]

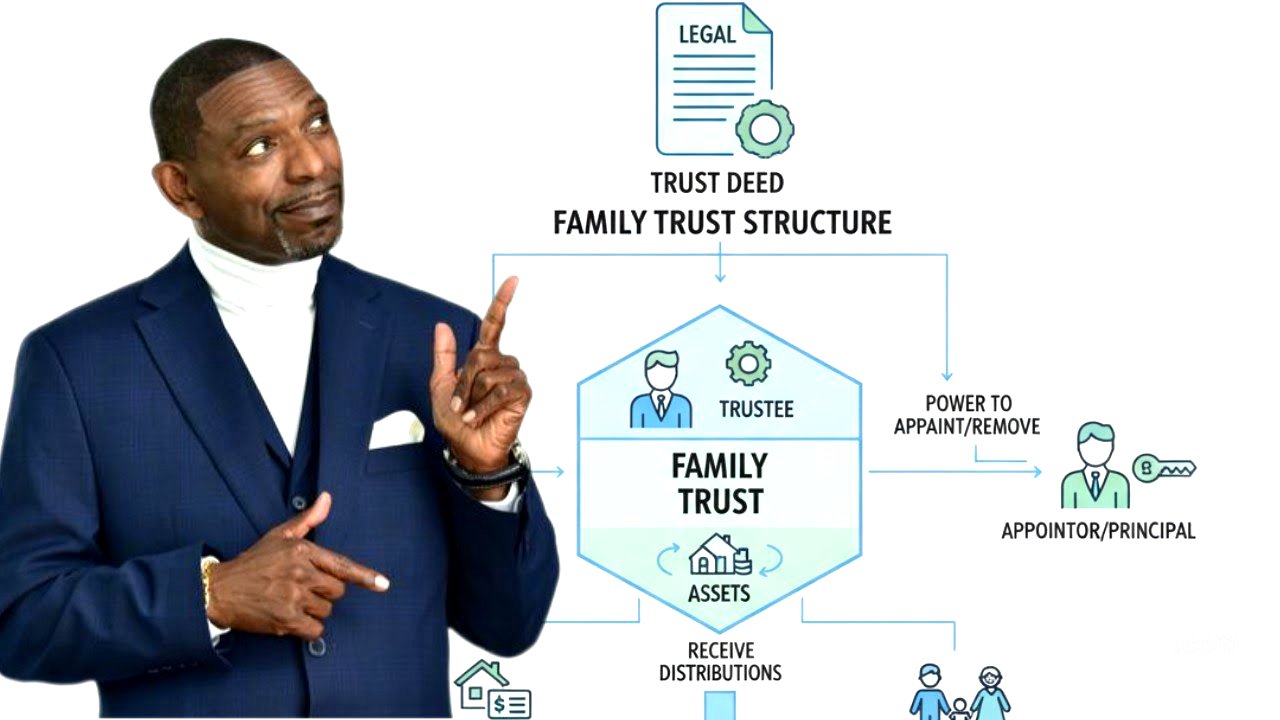

The initial step involves protecting your family through an irrevocable trust, which cannot be taken to court because it's not attached to you personally but to an Employer Identification Number (EIN). This structure ensures that the trust remains untouchable and that your wishes are followed after your death. The speaker underscores the importance of dealing with mortality to truly live and gain God's attention, as a good person leaves an inheritance for their children's children.

No Attachment: Irrevocable Trust [3:48]

Having an irrevocable trust means there is no attachment to you, protecting your assets from being contested in court. While revocable trusts offer some protection, they can still be challenged. The speaker advocates for complete detachment to ensure untouchability, emphasizing the hard work and sacrifices of previous generations to accumulate wealth. Operating under an irrevocable trust separates you from the "corpse" created by the social security number, offering freedom from the commercial system.

Co-Trustee: Recognizing the Anointing [6:55]

The next step is to appoint a co-trustee, someone you trust to manage the assets. The speaker stresses the importance of choosing someone who shares your values and has the "anointing," or divine favor, to ensure the assets remain blessed. He uses the example of David and Jonathan to illustrate a co-trustee relationship based on recognizing and respecting the anointing.

Successor Trustee: Passing the Legacy [15:40]

The third component of fortifying your family is selecting a successor trustee, someone who can take charge if something happens to both you and your co-trustee. This person should already be protecting something and be different from the crowd, indicating they are responsible and have integrity. The speaker encourages having "legacy conversations" with family members to discuss these roles and ensure the legacy is passed on responsibly.

Step 2: Funding Your Trust [31:59]

Funding the trust involves placing your assets inside it, which many people fail to do. The speaker uses Michael Jackson's estate as an example of what happens when a trust is not properly funded, leading to legal battles and mismanagement. He stresses the importance of having conversations about assets and how they should be distributed.

Tangible and Digital Assets [43:55]

The speaker details the types of assets that should be placed in the trust, including tangible assets like houses, cars, gold, and silver, as well as digital assets like cryptocurrency and royalties. He explains that buying cryptocurrency through the trust allows profits to be considered trust contributions rather than income, avoiding capital gains taxes. He advocates for shifting from tangible to digital assets to align with the future.

Life Insurance Policy [53:51]

The speaker advises against whole life, universal life, and index life insurance policies, calling them slow and a waste of money. Instead, he recommends buying a term life insurance policy with a large face amount and making the trust the beneficiary. This significantly increases the trust's net worth and provides a substantial benefit for future generations.

Step 3: Finance Your Future [1:00:21]

The final step involves structuring the trust to finance your future. This can be achieved by paying bills out of the trust, which creates a trust financial statement and builds a Paydex score (business credit score) with Dun and Bradstreet. The speaker explains that this financial statement, along with tangible and digital assets in the trust, can be used to secure loans from banks, which can then be reinvested through the trust.