TLDR;

This video summarizes Robert Kiyosaki's book "Increasing Your Financial IQ," which outlines five essential Financial IQs for building and maintaining wealth. These include making more money by solving problems, protecting your money from various predators, budgeting effectively, leveraging resources, and continuously improving financial information. The video uses stories and examples to illustrate each concept, emphasizing the importance of financial education and proactive problem-solving.

- Financial IQs are essential for building and maintaining wealth.

- Solving problems leads to increased income and financial intelligence.

- Protecting money involves understanding and avoiding financial predators.

- Effective budgeting focuses on increasing income and paying yourself first.

- Leveraging resources and continuously improving financial information are crucial for financial success.

Financial IQ #1: Making More Money [0:19]

The first Financial IQ involves increasing income by solving problems. Just as visiting a dentist solves a toothache, addressing money problems can alleviate financial strain. Solving problems, even personal ones like shyness or lack of knowledge, can improve skills and increase earnings. The more problems you solve, the higher your financial IQ becomes. Ignoring money problems leads to financial decline, so it's crucial to address them early. The process of solving problems makes you rich, and solving problems for others can lead to unlimited financial growth.

Financial IQ #2: Protecting Your Money [6:06]

Financial IQ number two focuses on protecting your money, measured by how much you keep. It's important to protect your money from financial predators, including bureaucrats, partners, lawyers, brokers, and businesses. Bureaucrats, through taxes, take a significant portion of your income, and it's essential to understand how different types of income (earned, portfolio, and passive) are taxed to minimize this. Partners, especially in marriage and business, require exit strategies like prenuptial and buy-sell agreements. Lawyers can be financial predators, so it's important to protect assets by keeping nothing of value in your name, buying personal liability insurance, and holding assets in legal entities like LLCs. Brokers, or salespeople, should be carefully chosen based on their interest in building relationships and their own investment practices. Businesses can also be predators if their products or services only make them richer, not you.

Financial IQ #3: Budgeting Your Money [16:54]

Budgeting involves coordinating resources, focusing on creating a budget surplus (excess of income over spending). Kiyosaki suggests increasing income rather than cutting expenses to achieve this. Increasing expenses that generate extra income, such as marketing, and paying yourself first are crucial. Paying yourself first involves allocating a percentage of your income to assets before paying other expenses. Kiyosaki and his wife hired a bookkeeper, Betty, to take 30% of their income off the top and put it in the asset column. Even when short on funds, they prioritized paying themselves first and then hustled to make more money to cover the remaining expenses.

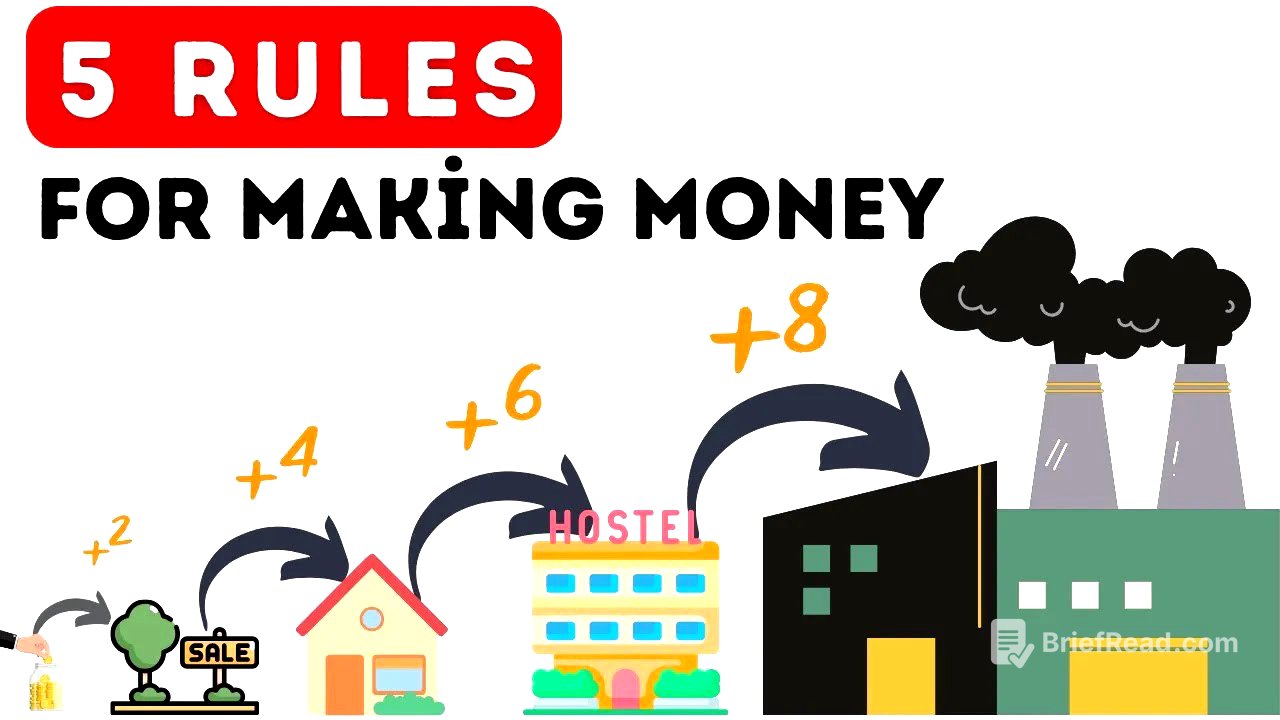

Financial IQ #4: Leveraging Your Money [23:12]

Leverage means doing more with less. Unlike putting money in a savings account, investing in assets like property with a bank's help provides leverage. Leverage is risky only when investing in assets you have no control over. Control over income, expenses, assets, and liabilities is key to applying leverage with minimal risk. Leverage extends beyond money to include products, other people's knowledge and time, and your network. Using other people's time by outsourcing tasks and leveraging your network by knowing the right people are essential for success.

Financial IQ #5: Improving Your Financial Information [27:17]

In business, information is crucial for financial success. Access to information can be a huge asset, while poor or mistaken information can be a liability. Many people struggle because they use outdated information. Information is abundant but also rapidly changing, doubling every 18 months, so continuous education and updating knowledge are essential. Using obsolete information is detrimental to financial health.